Over the past five years, we’ve witnessed an Atomization of the Seed Stage. Early fundraising is no longer a one-and-done fundraise of a single round of Seed capital subsequently followed by a Series A 12–18 months later.

Rather, it has been broken into bits of a series of capital raises to reach meaningful milestones… “pre-seed,” “post-seed,” and rounds in between have become the norm. A seed extension has ceased to be the equivalent of scarlet letter, and instead has become commonplace.

Whether or not this situation is good or bad for entrepreneurs and the ecosystem, it is indeed reality.

One of the results of this change is that Founders now approach Series A funds with increasingly varied histories.

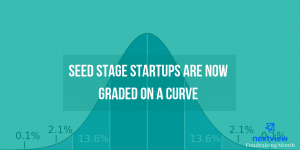

The bar for Series A has moved

The flood of seed-funded companies coupled with proliferation of seed fundswilling to underwrite incremental capital into new and existing portfolio companies, has yielded a broad backlog set of “seed startups” with wild variations across the following three dimensions:

1. How much time has elapsed since company founding.

2. How much total capital has been put into the company since founding.

3. (Effective) post-money valuation.

Once upon a time there was a “bar” for Series A — a threshold, once crossed would yield a positive successful fundraise (e.g. $100K in MRR was cited).

https://bettereveryday.vc/seed-stage-startups-are-now-graded-on-a-curve-15a4968e8534